Scaling Digital Banking Services: Why a Multi-tenant Model is the Credit Union System’s Key to Efficiency

Canada’s credit union system enters 2026 with a significant milestone: twenty-one consecutive years of ranking first in customer service excellence. This achievement, recognized by the Ipsos Awards Top Honours for Financial Services Excellence in Canada1, signals a deep, member-centric understanding that sets them apart from other financial institutions in the country. It also provides a strong foundation for continued leadership.

Yet this advantage is entering a new phase. Credit union member expectations have shifted rapidly toward digital-first engagements over the past five years. What began as a trend has now become the standard for how Canadians expect to bank. Digital channels can no longer be viewed as add-on to in-branch service. They are the norm. Members now expect the same personalized, member-centric experience across every interaction, including in-branch, mobile apps, online banking, and call centres.

Industry findings reinforce the magnitude of this shift. Payments Canada’s annual Canadian Payment Methods and Trends Report 2, mentions that digital payments represented 86 per cent of total payment volume of payments in Canada in 2024. Canadian Bankers Association 3 findings report 70 per cent of Canadians now use a banking app as part of their regular banking experience. These findings highlight the criticality of digital capability for member loyalty and a source of competitive advantage.

Beyond the rise of digital-first expectations, credit unions face additional headwinds that challenge their ability to maintain exceptional service levels. Profit margins across the system are tightening, and the industry is preparing for high-pressure milestones, specifically the initial phase of Open Banking and the launch of Canada’s Real-Time Rail in 2026.

These pressures are compounded by major banks and agile fintechs aggressively competing for the next generation of members. With their national reach, superior digital ecosystems, and rapid innovation cycles, these competitors are increasingly drawing younger customers away from the credit union system.

To address these challenges, the system must move beyond legacy, decentralized architectures that constrain the ability to respond at speed. Cloud-native, multi-tenant SaaS platforms offer a path forward, enabling institutions to transition from fragmented technology stacks toward a shared, scalable digital foundation. By distributing the costs of innovation, security, and compliance across the system, this model improves operational efficiency, protects margins, and reduces technical debt.

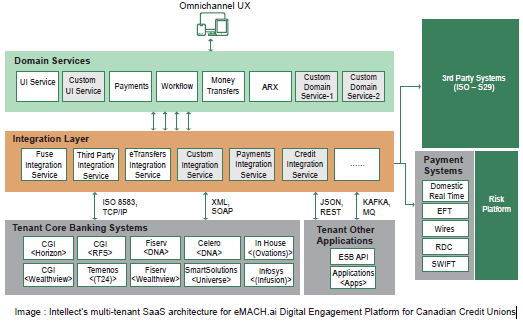

A Look Inside Multi-Tenant SaaS Architecture

We at Intellect have built a multi-tenant platform for our digital banking offering (eMACH.ai DEP) that allows multiple financial institutions to operate on a shared infrastructure with robust logical isolation. This multi-tenant SaaS approach creates a stable, enterprise-grade foundation for delivering consistent digital experiences through five core pillars:

● Unified platform layers: All tenants utilize the same core layers—including the UI, product microservices, and integration services—to ensure high asset reuse and accelerated innovation

● No-code configuration: Tenant-specific requirements such as branding, workflows, validations, and features are managed through configuration rather than custom code forks

● Secure data isolation: A shared database schema is employed alongside strict tenant guardrails to guarantee complete data isolation, security, and auditability

● Universal API framework: Common APIs support Retail, SME, and Corporate segments, which enables seamless scale without architectural duplication

● Continuous improvement: This shared ecosystem delivers a lower total cost of ownership, faster time-to-market, and continuous upgrades that improve resiliency and performance across all tenants

Image: Intellect’s multi-tenant SaaS architecture foreMACH.ai Digital Engagement Platform for Canadian Credit Unions

Unlocking the Value Pool: Quantifying the Opportunity

Independent analysis underscores the immense potential of system-wide scale. SATOV Consultants 4 estimates that accelerating digital and branch transformation could unlock $150 to $200 million in value across the Canadian credit union system. Currently, much of this value is trapped by decentralized technology environments that elevate costs and slow innovation. Transitioning to a shared platform model removes these constraints, allowing institutions to rethink their branch footprints in tandem with elevated digital engagement to create a more personalized member experience.

Reimagining the Cooperative Superpower

The credit union system cooperative model has always been a defining strength of the system; when paired with cloud-native architecture, it becomes a strategic engine for transformation. Shared governance and coordinated investment multiply the impact of every technology dollar by shifting the system away from the friction of parallel, disconnected efforts. This approach allows the system to solve technical challenges once and benefit collectively.

This unified strategy also improves compliance readiness and enables institutions, regardless of size, to offer advanced digital features. The result is a consistent, high-quality experience for members across Canada, reinforcing the system’s long-standing reputation for service excellence.

Strategic Execution: Beyond Technology

Delivering a multi-tenant SaaS environment requires capabilities that extend beyond simple implementation. Success requires partners who deeply understand credit union governance, regulatory expectations, and the operational realities of distributed networks. Experienced partners can accelerate delivery and reduce risk, helping institutions manage change while maintaining uninterrupted service.

From a strategic lens, success requires viewing platform transformation not as a technical upgrade, but as a fundamental reimagining of how an institution creates value. Unlocking measurable outcomes depends on ensuring that technology, operations, and governance teams are fully aligned around a shared roadmap.

| As of December 15, 2025, Intellect has partnered with Bulkley Valley Credit Union, Kindred Credit Union, Rosenort Credit Union, and League Data (representing 32 credit unions) to implement eMACH.ai DEP as a multi-tenant SaaS platform. |

The Path Forward: Positioning for a Digital-First Future

The industry’s record of service excellence demonstrates the enduring power of the cooperative model. The current challenge, and the greatest opportunity, lies in extending that advantage into the digital-first era. Cloud-native platforms provide the foundation to modernize at scale while preserving the local trust that members value.

Institutions that act now will shape the next phase of Canadian financial services. By reinvesting in their cooperative superpower through a shared digital foundation, credit unions will modernize with speed, protect their identity, and secure long-term growth in an increasingly connected future.

A perspective from The eMerge Quarterly editorial team

Partager