AI-first lending: redesigning the credit enterprise for the next decade

80% of the unstructured banking data still going unused. See how AI-first lending turns critical hidden information into a lasting competitive moat.

John Miller runs a mid-sized auto components manufacturing business. One of his key OEM clients doubles its orders, and he needs a $600,000 working capital line to procure raw materials quickly. He approaches his bank and submits financial statements, tax filings, bank statements, and projections—expecting a timely decision.

Inside the bank, the file begins its slow journey. Data is extracted from documents and re-entered into internal systems. Financial ratios are rebuilt in spreadsheets. Queries move back and forth between the underwriter and the relationship manager, creating multiple versions of the same document. Phone calls resolve key questions, but much of that context is never captured in the system. What should take days stretches into a week.

For John, the impact is delayed access to credit and strained supplier commitments.

For the bank, the consequences are broader. In origination, slow turnaround leads to lost business and poor customer experience. In underwriting, manual assessment reduces first-time-right quality and weakens risk visibility, increasing delinquency risk. In servicing and operations, fragmented systems reduce efficiency. In collections, delayed signals impair recovery outcomes.

Most banks today have digital loan systems in place. But the constraint is no longer digitization—it is the lack of intelligence within the workflow. Until lending evolves from simple process routing to true intelligent orchestration, friction will persist across the lending lifecycle.

In lending, AI-first is not an overlay but a structural redesign across origination, decisioning, servicing, and collections. Competitive advantage will come from building an “Enterprise Knowledge Garden” that transforms tacit knowledge into a compounding intelligence layer.

Reimagining lending customer acquisition journey with AI

The lending process has evolved significantly over the past two decades, driven by the adoption of digital technologies, advanced analytics, AI, APIs, and automation. These innovations have delivered substantial business impact for lenders and national economies.

While these innovations have enabled new channels, most improvements have focused on existing offerings and processes. Today, AI has the potential to fundamentally disrupt the loan acquisition process, and this is where leaders will focus their efforts.

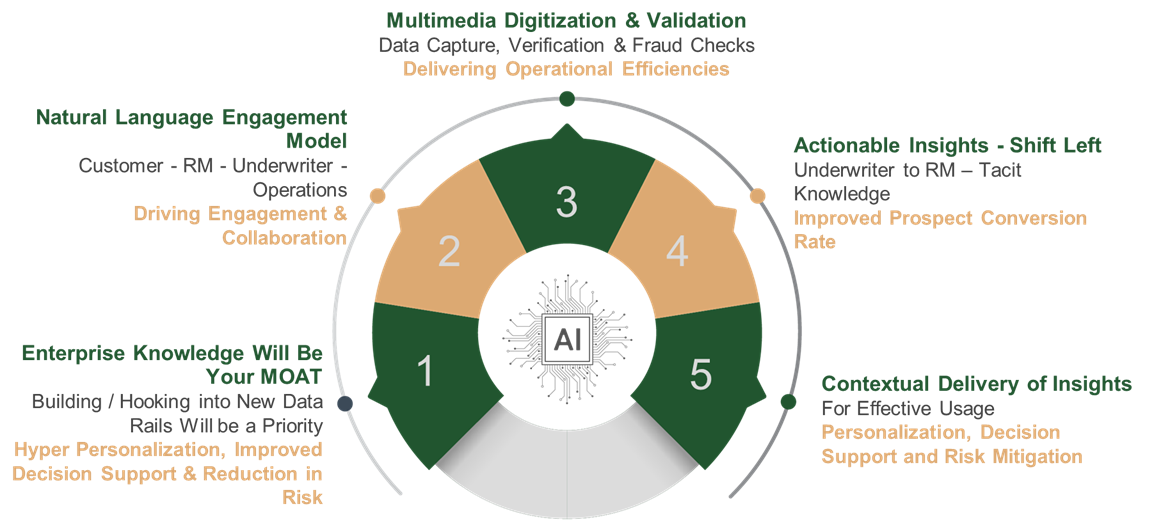

AI first disruptions in lending

Enterprise knowledge will be your moat

AI requires extensive information. Banks hold ~80% of their data in unstructured formats (audio, video, emails), with only 3% of organizations actively evaluating it — leaving the vast majority of potential insight untapped. Enterprises must unlock implicit and tacit knowledge within the organization and establish new data channels. The ability to access untapped and emerging information sources will distinguish leaders from laggards.

While connecting to public digital infrastructure and shared data ecosystems is essential, it will not be the main differentiator, as it is available to all industry players. True differentiation will depend on how effectively organizations leverage AI to use the unstructured data. Enterprises should integrate these insights and expand beyond traditional banking ecosystems. For high-value segments such as SMEs, banks can orchestrate ecosystems with services such as invoicing, expense management, accounting, and taxation. This approach enhances customer retention and provides deeper business insights for personalization, pricing, and risk management. For non-priority segments, such as education, banks can participate in third-party ecosystems, which may offer less granular insights but still provide more information than traditional sources. The foundation of the AI-first model will depend on how banks and lenders develop their Enterprise Knowledge Garden.

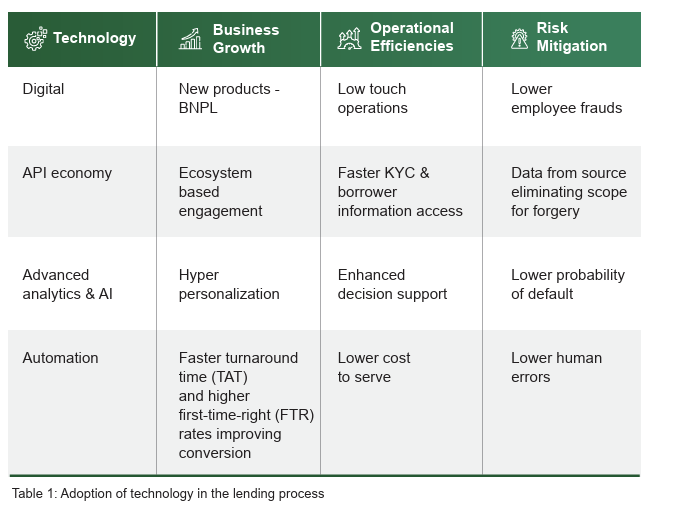

Business impact – business growth and risk mitigation

Structured & linear workflows to unstructured & contextual conversational engagements

Current lending processes are highly structured and linear. While this works for simple products like personal loans or BNPL, it creates overhead and redundancies for complex products such as mortgages or small business loans, which involve multiple stakeholders. Digital Experts simplify such complex lending journeys by the embedded intelligence across every stage of the lifecycle. In origination, they accelerate onboarding through automated document extraction and the ability to process unstructured application inputs. During underwriting, they enable comprehensive risk assessment and intelligent summarisation to support stronger credit decisions and lower NPA risks. Beyond disbursement, they enhance customer service through autonomous query resolution and strengthen collections with AI-enabled case allocation and persona assistants to improve recovery outcomes.

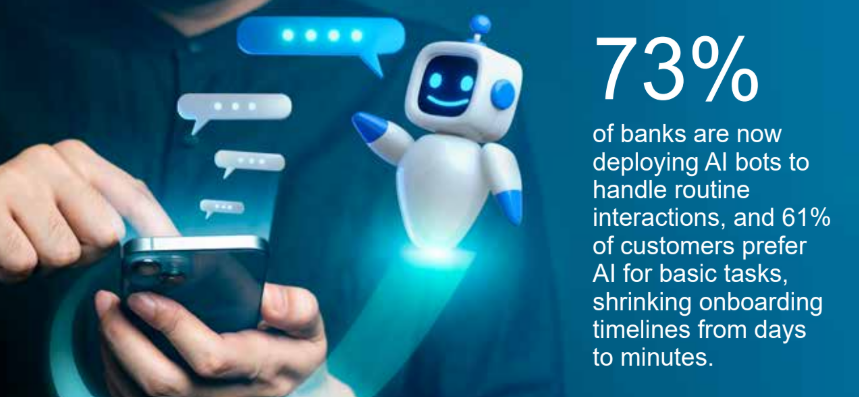

However, banking has now evolved from manual, high-cost human servicing to scaled chatbot automation, with 73% of banks now deploying AI bots to handle routine interactions. Today, AI adoption has further evolved with AI-first models enabling intelligent, context-aware engagement — 61% of customers prefer AI for basic tasks, and onboarding timelines have shrunk from days to minutes. AI enables hybrid models that overlay group conversations among all stakeholders, allowing for unstructured and contextual engagement. This approach accelerates response times, improves information flow, and increases conversion rates. Additionally, it captures tacit knowledge shared during interactions, which can further enhance decision support systems.

Business impact – business growth & operational efficiency

Multimedia insight generation

Banking has evolved from structured, email-based interactions to conversational channels such as chat and voice, with 70%+ of customers now preferring digital conversational engagement. As these interactions grow, banks must extract insights not only from documents and emails, but also from contact center recordings and video conferences — converting conversations into institutional memory and reducing knowledge loss from workforce turnover. Institutions leveraging conversational AI with enterprise context have reported up to ~60% reductions in average handling time and customer satisfaction improvements of up to ~50%, demonstrating the tangible impact of contextual, intelligence-driven engagement.

Business impact – protecting institutional memory while improving customer satisfaction

Actionable insights – shift left

AI in credit risk assessment reduces the time to approve loans by 50-60%. When relationship managers receive predictive insights upstream, this further strengthens applications before they reach underwriters, reducing friction and enabling higher effective throughput without adding headcount. Many loan rejections could be avoided if relationship managers had insights into underwriter decisions. Providing timely insights and recommended actions enables managers to help borrowers strengthen their applications, improving conversion rates. Delays in remediation from underwriters can result in lost opportunities in today’s competitive environment.

Business impact – improved prospect conversion rate & operational efficiency

Key imperatives for leaders to scale in the AI-first landscape

The AI paradigm is clearly disruptive. Leaders must focus on four key layers to scale AI-first lending and ensure effective adoption throughout the lending journey.

- Intelligence infrastructure: Organizations should leverage curated knowledge frames to power digital agents, including institutional ontologies, policy logic, and decision scaffolds, to analyze and simplify workloads. This approach improves efficiency and reduces errors. Leveraging internal and ecosystem data provides early warning signals and behavioral patterns beyond credit ratings, while accessing new data channels as they emerge. An open architecture is essential for data and model interoperability, enabling seamless integration and multi-model orchestration.

- Trust and protection layer: It is essential to ensure data security through compliance with global and local data protection regulations (e.g., GDPR and equivalent regional frameworks), and sectoral norms, as well as implementing encryption, masking, and data lineage. Building a trusted ecosystem requires both compliance and stakeholder confidence. AI systems should also operate with role-based entitlements, maintaining consistent control across users and automated agents.

- Governance and human oversight: Strong governance ensures AI-driven lending is defensible, explainable, and operationally sound. Human oversight is necessary for judgment in outlier cases, such as underwriting exceptions, and for maintaining auditability and traceability. This layer reassures boards and regulators that efficiency improvements do not compromise reliability.

- Enterprise operating model & strategic moat: Organizations must take a holistic approach, viewing this as a strategic partnership and establishing guardrails for technological advancement, rather than simply procuring technology. Over time, a strategic moat will be built from protected enterprise knowledge, data assets, and embedded decision logic.

These four layers are interdependent and must be designed and managed together. While generating deeper insights is important, delivering them to the right stakeholder at the right time in the acquisition process is even more critical. Insights should be integrated contextually into the process to ensure effective adoption.

As AI matures, the gap between leaders and laggards will widen, with success determined by agility and adoption strategy.

Conclusion: the strategic mandate for AI-first lending

The transformation underway in financial services is not incremental — it is architectural.

Over the past two decades, digital technologies improved access, distribution, and efficiency. The next decade will be defined by intelligence—how banks unlock enterprise knowledge, convert unstructured data into institutional memory, and embed contextual reasoning across lending.

In lending, AI-first is not an overlay but a structural redesign across origination, decisioning, servicing, and collections. Competitive advantage will come from building an “Enterprise Knowledge Garden” that transforms tacit knowledge into a compounding intelligence layer.

AI-first models replace linear workflows with contextual, conversational engagement—accelerating decisions, reducing friction, and capturing reusable insights. By embedding predictive intelligence early in the process, banks improve application quality, increase conversions, and scale underwriting without proportional headcount growth.

AI-first lending with PF Credit

With PF Credit, powered by Purple Fabric and optionally integrated with eMACH.ai Lending, intelligence is embedded across origination, underwriting, servicing, and collections – not as automation, but as real-time reasoning and continuous knowledge compounding.

The outcome is measurable and structural: faster and higher-quality origination, sharper risk calibration, lower operating costs, stronger recovery performance, and reduced portfolio volatility. In an environment where speed, insight density, and risk precision define profitability, AI-first is not a feature layer. It is the foundation of a more adaptive, resilient, and performance-led lending institution.

Book a meeting with our subject matter experts now for a deeper discussion on how PF Credit can support your organization’s lending transformation. We look forward to continuing the conversation and supporting your journey toward AI-first lending.

Author:

Vivek Patil,

Chief Growth Office,

Consumer Banking, Intellect Design Arena Ltd.

Share