Credit Unions

Creating a high-touch digital experience

without limiting the personal touch

Empowering Lifestyles for

Credit Union Members

At the heart of every credit union is a mission to serve members with care, integrity, and innovation. iGCB understands the unique challenges you face—creating meaningful connections while driving growth, managing costs, and mitigating risks. Our solutions empower credit unions to deepen member relationships through personalized, seamless experiences, unlock new revenue streams with modernized services, optimize operational efficiency to control costs, and proactively address risks with intelligent, integrated tools. Together, we can reimagine the future of your credit union, where every interaction builds loyalty, fosters growth, and ensures long-term success.

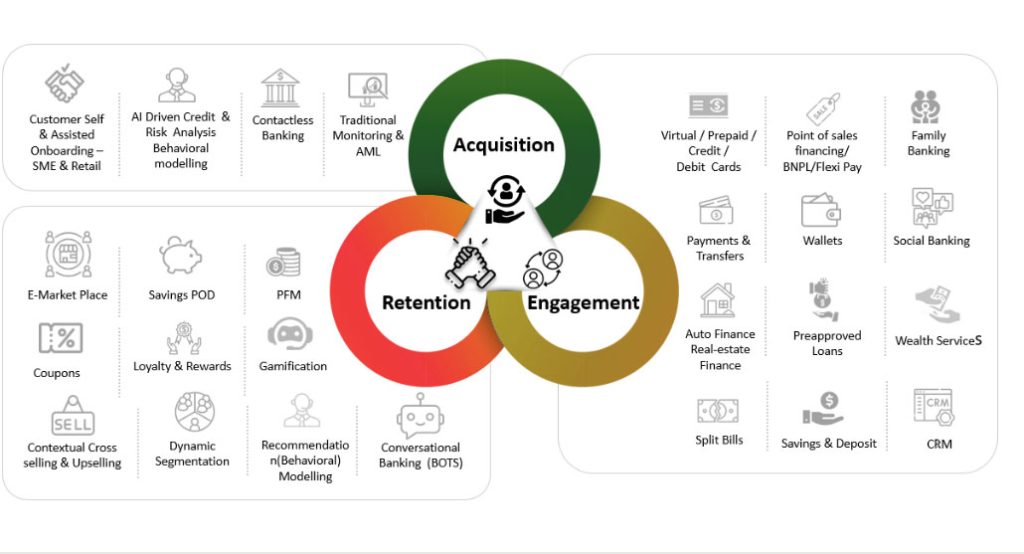

One platform – 3600 Engagement

Best Fit for Credit Unions

eMACH.ai DEP

Unified Digital Engagement Platform that helps Banks and Credit Unions offer a seamless, contextual engagement across the entire customer lifecycle—from acquisition and engagement to retention

What Our Clients Say

Transforming

Challenges into

Success Stories

Boosting Branch Efficiency by 70% with eMACH.ai DEP for One of the Largest Banks in the Arab World

70% boost in branch efficiency

4-month rapid build for digital teller

Core-agnostic, multi-currency branch platform

Faisal Islamic Bank of Egypt accelerates its Retail Banking Transformation journey with eMACH.ai Digital Engagement Platform

Case Study: A top UAE Bank cuts SME onboarding time by 98% with eMACH.ai Digital Engagement Platform

Case Study: A leading bank in Tanzania improves customer experience & revenue with Core, lending & digital channel transformation.

Award-Winning

Innovations

Best Digital Banking Platform award by Fintech Future Banktech Awards 2025 to eMACH.ai DEP

Digital Banker award for Best Retail Banking Loan Software for Dukhan Bank

Recognized as a Leader in five quadrants in the Chartis RiskTech Credit Lending Operations Solutions 2025 report

Featured among 26 global vendors in Celent’s Decoding Small Business Digital Banking Platform report for Functionality and Technology Innovation

Intellect Design Arena Played a pivotal role in shaping two of Forrester’s latest Trends and Vision reports on the present and future of Digital Banking Experiences

Ranked no.1 Retail Banking in IBSi Sales League Table 2025

Ranked no.2 Lending Retail in IBSi Sales League Table 2025

Explore.

Learn.

Innovate.

-

Islamic banking faces dual compliance challenge, says Intellect CEO Rajesh Saxena

NewsApril 29, 2026 -

Myanmar’s Ayeyarwady Farmers Development Bank Public Company Limited selects Intellect’s eMACH.ai Core Banking to drive end-to-end transformation at the Bank

NewsApril 24, 2026 -

Khalsa Credit Union, BC, Canada selects Intellect to power its next-generation digital banking platform

NewsApril 21, 2026